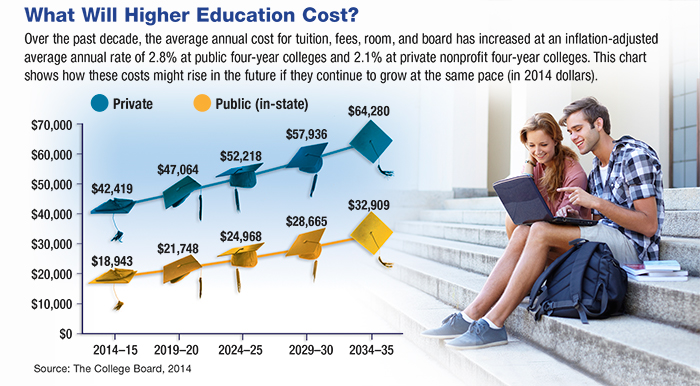

New Flexibility for College SavingsThe steady rise in the cost of a college education has slowed somewhat during the past two years. At public four-year schools, the average inflation-adjusted cost of tuition, fees, room, and board increased just 1.2% in the 2013–14 academic year and 1.0% in 2014–15. At private schools, the increases were 1.8% and 1.6%, respectively.1 That’s good news for families with current or future students. But even so, college is expensive, and the long-term trend suggests that costs may rise at a faster pace in the future (see chart).

Despite the cost, higher education is a valuable investment. College graduates not only earn more than non-graduates but tend to be healthier, more satisfied with their jobs, and more likely to remain employed during tough economic times.2A strategic savings plan could be a key step toward providing your student with the many benefits of a college diploma. Section 529 Plans The funds in a 529 savings plan accumulate on a tax-deferred basis and can be withdrawn free of federal income tax when used for qualified education expenses at accredited post-secondary schools, such as colleges, universities, community colleges, and certain technical schools. Qualified expenses include tuition, fees, room and board, books, and supplies. Section 529 plans feature high contribution limits (set by each state), and there are no income restrictions for donors. Each 529 plan has its own rules and restrictions, which can change at any time. As with other investments, there are generally fees and expenses associated with participation in a 529 savings plan. There is also the risk that the investments may lose money or not perform well enough to cover college costs as anticipated. The tax implications of a 529 plan should be discussed with your legal and/or tax advisors because they can vary significantly from state to state. Most states offer their own 529 programs, which may provide advantages and benefits exclusively for their residents and taxpayers. Before investing in a 529 plan, please consider the investment objectives, risks, charges, and expenses carefully. The official disclosure statements and applicable prospectuses — which contain this and other information about the investment options, underlying investments, and the investment company — can be obtained from your financial professional. You should read this material carefully before investing. 1–2) The College Board, 2013–2014 |